How Do You Know It’s Time To Hire Your First Employee?

I’ve been working with "James" for about one year now. James is the CEO of a really cool company. Over the past year, I’ve had the pleasure of watching James grow his business to a pretty substantial level. Now, it's finally time for James to hire his first employee.

There’ve been the usual growing pains that any business goes through. You have growth issues, you have contractor issues, and you have collection issues just like any other business.

[Do you want to grow your business? Maybe I can help. Click here.]

And, there’s the constant push and pull between funds available and growth. Managing cash is especially important when you’re bootstrapping like James.

We reviewed the plan in December. It was clear, as part of the plan, James was going to be adding teammates to the team.

The question was when should he pull the trigger?

Every founder goes through the issues James faced. If you hire your first employee too early then you are burning valuable cash. If you hire your first employee too late, then you can stunt your growth.

It really is a balancing act.

You’ve Gotta Have A Plan.

Sometimes you just wing it. You just say, “Hey, we could really use some more help, so I’m just going to hire this person. I know we can’t afford it, but I’m going to hire this person anyway.”

And then, six months later, revenue doesn’t grow like you hoped it would, and you don’t have as much money as you expected. Now you’re really in a bad place.

And that’s why having a financial plan is so, so important. It’s not difficult for you to put together a simple financial plan either.

So, let’s get started.

You’re going to need to gather up everything to do with your company. Let’s break this into two parts:

- Revenue:

- Your revenue by month

- Your expected revenue by month

- Your current cost of goods (if you are selling a physical product)

- Your future cost of goods

- Your Expenses:

- Your salaries for each employee, including yourself

- The expected salaries you’re going to pay future employees

- Your rent

- Your insurance

- Subscriptions

- Office supplies

- Advertising expenses

- Travel expenses

- And anything where you are spending money to run your business

A word of warning.

Many people make the mistake of not truly accounting for all their expenses. I think they do it to give themselves the feeling that things are better then they really are.

You can’t make that mistake. You really need to know exactly where you stand. You do this not so you can punish yourself. You do this so you know how to responsibly plan going forward.

Completing this simple exercise puts you ahead of 80% (maybe 90%) of the businesses out there, so congratulations.

Now what?

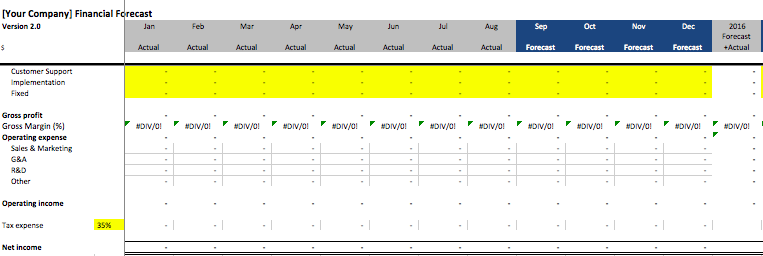

Put everything in a simple spreadsheet. I recommend using separate tabs for each individual category. Then, you should have each category feed in to a master spreadsheet.

The final result will look something like this:

Congratulations. You’ve just built an income statement for your company. More important, you’ve built a model for the future growth of your company.

Now, you’re in control of your business. You now know:

- How much cash you’re going to need to grow your business, and…

- Exactly where the cash is going, and…

- How many employees you can hire, and…

- When you can hire the employees, and…

- How to have complete visibility of the financial picture of your company.

This is all well and good, but what happens if you don’t hit your plan?

Do you want to go a step further? It won’t cost you much time.

Great. Let's do it.

One of the smartest things you can do is develop a few different plans:

- A worst-case plan

- A medium-case plan

- A best-case plan

The benefit of having a few different plans is you’ll be ready to pivot (positively and negatively) depending upon what happens.

Let’s say things are going really well. What should you do? Now you already have a plan in place that you can use to guide yourself.

Let’s say things don’t go as well as planned. Well, you have a plan ready for that case too.

The beauty of having these simple plans completed ahead of time is you won’t have to develop them in a panic. You’ll be completely prepared and calm.

And, the more prepared and calm you are, the more likely you are to make good, rational decisions.

There’s one more important thing you need to know about developing financial plans. You will redoing your financial plan at least every year. As your business grows, resetting your financial plan is the best way to stay in control of your future.

Here’s the thing. Growing a business takes cash. And managing your cash (whether you’re bootstrapped or venture backed) is a critical discipline on your journey to success.

What if you're way off your financial plan?

Don’t worry. It’s very normal you to be way off. This is especially true if you’ve never done this before.

You’ll get better the more you times you go through the process. The most important thing is just getting started.

Back to James…

James set his plan in place. He included in his budget the expenses, and timing, for hiring new employees.

The business kept growing and the time came for James to pull the trigger on hiring his first employee. James already had recruited his new employee. In fact, the employee was already working for James part-time.

However expenses were higher than expected in some areas, so there was less cash than expected. What should James do?

By the way, it is normal for expenses to be higher than expected. It happens. But James could manage the situation from a place of strength because he had a budget.

James could objectively look at the data and make an objective decision.

James decided to wait a month before bringing on the new employee full-time. Delaying the new hire would mean James would have to carry the extra load himself. However, it also meant he would be in strong cash position going forward.

James did one other really smart thing that you should do too. He communicated honestly with his new employee why he was delaying bring him on.

Now James' new employee has started, and he is killing it!

Good for James and his new employee!

For more, read: What Are The 11 Painful Things You Need To Do As CEO?

Do You Want To Grow Your Business? Maybe I Can Help. Click Here.

Picture: Depositphotos